7 Financial mistakes you will certainly regret when you turn 50

For a common man, investment just happen. Every working professional becomes an investor for sure at some point during his / her career. It could be

- By buying tons of insurance policies just because your father also bought when he was young

- By becoming elite member of a famous get rich quick Ponzi MLM scheme – where only elite and selected few are invited to join. You join this because one of your highflying and partygoing neighbor has selected you to be a part of high flying life.

- Opening some fixed deposits and some recurring deposits as one of the senior coworker is doing the same.

- By buying some land miles away from town, purely going by the words of the land developer that the piece will be worth 100 time after x years

Here we see that investment choices are highly influenced by external factors. This external factor could be our family member, coworker, media – digital / print / TV, so called experts or relationship managers from our bank etc.

A common man, influenced by external factors take financial investment decisions. I am going to discuss a few of the financial mistakes made by common man which he will regret once he turns 50. This common man could be YOU – reading this post.

These mistakes you will certainly regret when you turn 50

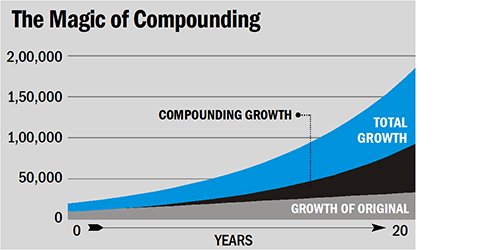

Delaying investments

When it comes to decision making about finances and investments, most of us like to postpone it to some other day. This stands true not only for decision making about investments but also for evaluating existing finances.

If you think that you will invest once you have sufficient money at a later date – You are WRONG. Believe me, the later date will never come in your life. The more you delay, more you will lose on the benefits of compounding.

Delaying investments? It can cost you DEARLY

The magical power of compounding

Not taking any risk with investments

For most of us, investing means opening up a fixed deposit or buying an insurance policy from some relative or a friend. While investing we never check for the real rate of returns or the cost of investment we are making. This ignorance results in the earnings which are far below the inflation rate and highly taxed. Though we do investment, but it results in a loss for us as the net gains usually are less when you figure out inflation and taxes in the earnings.

It is indeed surprising that even young working professionals resort to insurance and term deposits as an investment. When you have age in your favor, you must look to invest into equity through various channels.

Investments in equity will fetch far better returns over a long period compared to the money invested in term deposits and insurance. You can not create a sizeable retirement corpus without the help of equity exposure.

You do not have to be an equity expert to invest in equities.

Want to enter equity markets? Index based ETF funds are the safest bet

When you should start investing in stocks?

Not diversifying the investment

Diversification of investment is a common practice where your investments are spread across different asset class such that your exposure to any one asset class is limited. In other words you are not dependent on only one asset class to give you returns. This saves you from extreme swings in your net-worth in case of any financial turmoil in the economy.

When you do not diversify, you are unable to take advantage of the better performing asset class. Broadly speaking there are asset class like stock market, Government bonds, bank deposit schemes, commodities, real estate. At any given point of time , certain asset class will be giving better results than the other – based on the market economics. When you diversify, you need not to keep looking at your investments constantly and can sit and relax in peace.

Imagine during a bull run if you place your entire money in stock market and suddenly one day the market crashes and by the time it settles down you are down by 30%-40% on your principal. So no diversification is a big threat to your hard earned money too.

Why I need diversification of investment?

Falling prey to dubious / MLM investment schemes

We must accept that we are greedy and our investments are also greed driven sometimes.

We have seen in the past – many ponzi schemes come and go. They do not make anyone rich but most of the investors are left with no money when the scheme suddenly disappears.

Speak Asia, questnet and many such schemes are example where people have invested huge sums and lost their entire investment in no time.

There is no fool proof quick rich scheme which exists. If someone promises this to you, it’s a big trap. This is also true for get rich quick MLM schemes. When you invest, do some logical postmortem of your investment instrument. And always be skeptical about get rich quick and MLM schemes.

Mixing investment with insurance

Life Insurance covers your life and safeguard your dependents. Health insurance helps you in emergency situation where in you have to undergo some expensive medical procedure. So the term “insurance” assures you that in case of any unexpected emergency – insurance company will take care of you or your dependents.

The moment you try to mix insurance with investment – you are headed for something which is not right for your portfolio. Insurance linked investments can cost you heavy in the short term as well as long run. The thumb rule is not to mix insurance with investment but still millions of policies are bought every year – just for sake of investments or for sake of taking last minute tax benefits. These policies not only gives below par returns but also force you to have long term lock in. you can not get out of them as the exit costs are very high.

Also by investing in insurance linked investments you are locking your precious capital which can be used to generate much better returns.

Why you need Insurance ?

Not taking adequate insurance

Why you need insurance?

You never know what is going to happen in near/distant future. If someone is the only earning member of a family and due to health reasons, he is unable to work, or due to sudden demise of the sole earning member, family goes in no earning mode.

- Who will pay the EMIs of home loan, vehicle loan?

- How the monthly household expenses would be taken care of?

- How to pay kid’s school fee & tuition expenses?

- How to pay expensive nursing care? Hospital expenses are skyrocketing these days.

Do not assume that you need to buy insurance policy just because your friend who is a salesman in insurance firm told you to do so. First identify purpose of buying insurance. Assess your requirements, do your research properly and make sure that you are adequately covered with insurance for Your life and your health.

Not having an emergency fund

In personal finance and money management, emergency fund is the first line of defense against the unexpected problems in life. Financial emergencies can happen anytime, and most of the time they occur without warning.

- What if your car needs immediate repair?

- What if you are out of job for a couple of months?

- What if you broke your leg while playing gully cricket?

- What if a sudden voltage surge damaged your TV/Fridge/AC and all devices?

- How you are going to tackle this?

One must have a sufficient emergency fund to tackle any emergency situation. This fund can be parked in any accessible liquid mutual fund which can give you good return and you can access it pretty quickly when the need arise.

What is an emergency fund? And why you should have one?

So instead of being sorry when you turn 50, TAKE CHARGE or your finances. Be active and start investments for your needs.

Happy Investing !!!

Recent Comments