Want to enter equity markets? Index based ETF funds are the safest bet

Want to enter equity markets? Index funds are the safest bet

Most of us do not invest in equity markets because

- We are afraid of stock markets as we do not know how they work

- We think we do not have enough money for investments

- We think that investment is something which is to be done when you are nearing retirement

- We think we do not have basic education to invest money in stocks

All have investments in mind but we love to delay it due to reasons best known to us. We all know that we have to accumulate enough retirement funds as we need regular income when there is no salary for us. Still we try to avoid investing money.

It has been historically proved that stock market gives the best returns on your investments. If one is looking to create a retirement corpus, stock market can not be ignored as the returns generated through them beat the inflation by a good margin.

If you do not know anything about equity markets, if you have never invested in equity markets / funds, still you have one option which is quite safe and which does not require you to be an equity market expert. It is INDEX based Exchange Traded Funds. Index funds have consistently outperformed markets and so called equity experts if you look at a longer duration. In fact one of the richest fellow in the world and a great investor Mr. Warren Buffet says “Consistently buy an S&P 500 low-cost index fund. I think it’s the thing that makes the most sense practically all of the time. Index funds make the best retirement sense ‘practically all the time’“

So what are index Funds?

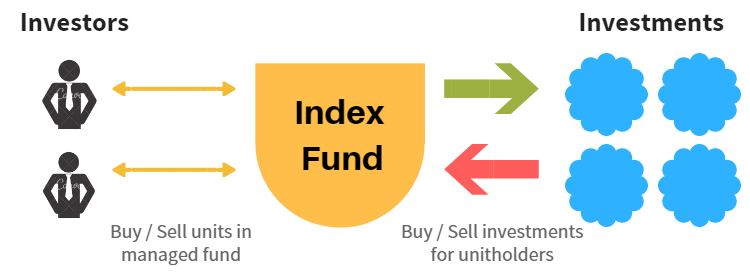

By definition, an index fund is a type of mutual fund with a portfolio constructed to match or track the components of a market index, such as the Standard & Poor’s 500 Index (S&P 500), BSE or NIFTY. An index mutual fund is said to provide broad market exposure, low operating expenses and low portfolio turnover

So what makes index funds safe as an investment instrument in equity markets?

- Index fund is a way to avoid the risk that comes with picking of individual stock: Index fund spreads out your investment into the stocks which are top performing on any equity index. This way you are not buying individual stock, but a set of stocks which are like top performers of any equity market.

- It helps you to buy not “the top company” but it lets you buy all top companies at a very low cost.

Costs matter a lot in the investment scenario. Most of the equity diversified funds charge a fund management cost of 2.5%-3.5% per year. In comparison to this, index funds usually have fund management cost of 0.5%-1% per year. So when you invest in index funds, you are already ahead of any equity diversified fund by 2%-3% and anyone who knows a little bit of arithmetic can say that over a period of 20 years this can make a huge difference in investment corpus.

Then why ETFs are not recommended by investment advisors / financial planners?

When you talk to an investment advisor, his or her salary is linked to the income they generate for the fund houses. More the fund management charge, more their salary. So it’s obvious that they would recommend top ranked funds which has more fund management charge than the plain vanilla index based ETFs.

There are no free lunches so anyone unless he has a personal interest can not give you honest advice regarding your investments.

So what is the recommendation regarding index based ETF?

As pointed out by investment mogul Warren Buffet –

- Start buying index based Exchange Traded Funds (ETF)

- Buy them every month through Systematic plan

- Stay invested in them for a very long duration

- You can bank on index based ETFs for your retirement plan

- When markets are battered or down – do not panic, keep investing regularly. This will help you average your cost of investment.

If you stick to the points mentioned above, you do not have to worry about your retirement corpus.

So with index based ETFs:

- You are saved from headache of actively managing stock portfolio

- ETFs give you exposure to the gains of stock market over a long period.

- You can plan your long term corpus goals for retirement / kids education with ease through index based ETFs

- You can keep the cost of your investments low through ETFs.

Happy Investing !!!

Recent Comments