Thumb Rule for any Retirement plan – Remember Your money has to outlive you

“Always remember – Your money has to outlive you”

Interesting sentence. But why do I need to worry about this? All our forefathers never worried about this so why should I break my head over this?

Things were different till last generation. Till a couple of generation back, things were pretty cool. Life was quite easy, you work for 30-35 years with any corporation and you retire with a regular pension amount per month which could take care of your day to day living. Families were joint and there were grownup kids to take care of you during your retirement years. Medical care was not expensive and life was relatively easy.

Yes, you are right. Things have changed drastically in this generation. Can you let me know what else has changed?

- Life expectancy has increased by about 20%- 25% in this generation. This means you will need to spend more years on this earth and that too of your old age.

- It doesn’t take rocket science to arrive at the conclusion that healthcare costs have skyrocketed in last few years and they are expected to climb more

- Cost of living – day to day expenses have increased with more exposure to urban living. Similarly cost of services have also increased at a steady pace.

- Biggest change is the family structure. Families are no longer joint families. Due to migration to urban areas families have become nuclear families and aged ones does not have a chance to live with grownup kids in their dusk years.

This sounds scary. What can I do to tackle this situation and have a comfortable life after retirement?

Yes this is scary for many of us too. As per many research reports, it is said that about more than 50% people who are about to retire are not in position to retire due to insufficient savings in their retirement funds.

There is no shortcut or a quick fix solution to this issue. You need to take comprehensive approach towards your retirement right from the beginning so that you can avoid retirement blues. As an employee you spend your life in helping company to enhance and balance their balance sheets, now it’s time you also think seriously to work on balance sheet of your life.

Ok, now help me out and tell me how can I get control over my retirement finances?

Below are several steps to take in order to make your money outlive you. These steps are simple to execute and if one takes these steps then he/she will be able to head towards a comfortable retirement financially.

- Make a proper plan

It is said that planning is the most important task to do anything. If there is proper planning then things bound to fall in place. Plan, Plan and again plan. Also at any stage of life, do not hesitate to go back and re plan if you think a particular strategy is not working. Have your plan written on paper so that you can constantly monitor and update it when required.

- Plan your investment portfolio

- Plan the asset allocation at different life stages

- Plan the savings/investment targets by age

- Plan your career in order to maximize your earnings

- Always aim for a bigger retirement corpus fund than you have planned

In any pan there is always room for some uncertainties. Always keep a buffer for uncertainties and go for at least 1.25 or 1.5 times of the nest egg you have planned for retirement. This will help you to sail through any hurdles that comes in your path while contributing towards your nest egg.

- Plan to work a little longer

This does not mean to toil even after your retirement. Idea is to work a little more – may be as a consultant on a part time basis for few more years so that the transition from active work life to retired life is smooth. This additional work will also help you to amass little more corpus fund for the retirement.

BUT consider this only if you feel like working as during the end of professional life very few would like to work for some more time. - Take adequate health cover

It is easy and cheaper to take health cover at young age. Evaluate various service providers and take appropriate health cover so that you don’t have to shell out money for medical reasons. Remember – health care costs have already skyrocketed and are set to increase further. - Get rid of all debts as soon as possible

As I had discussed earlier too, try to avoid consumer debt, personal loans and any other loan as it costs money to service loans. Mortgage/home loan also try to complete sooner than its tenure so that you have sufficient free money for investment targeting your retirement. Any debt is a hindrance in wealth creation. - Do not forget inflation in your plan for retirement

Inflation is a termite which constantly eats up your money and reduces its value. When you plan for investments, retirement corpus fund do consider the inflation. Inflation factor must be considered so that you achieve your target corpus fund without any surprises midway to retirement. - Re-look at your plan every year

By doing this you can evaluate your progress and take corrective action. Remember for any long term plan you need constant evaluation-feedback-corrective action cycle in order to maximize the chances of its success. - Budget – Budget – Budget

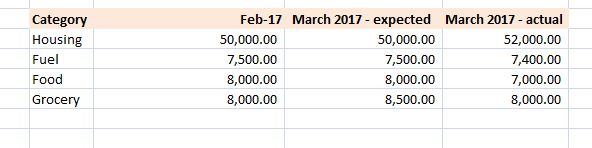

Note down every expense daily – month by month (how to do it). It doesn’t take much time but it ensures that you plug money leaks. Money leaks can prove deadly and unless you write expenses you will never come to know where your money is leaking. Budgeting also helps in proper funds allocation to investments which in turn will help in creating a good retirement corpus fund.

Once you diligently follow the 8 steps listed out above, you will have a better control over your retirement finances.

If you still find things not getting better at retirement age, do not hesitate to look for reverse mortgage option. You have paid monthly payments for a good period of your life towards your home, why not capitalize it through reverse mortgage. This will give you sufficient money for day to day expenses.

One final word, if you are alone or feel you could be burden to your kids, plan well ahead for a care home for elderly. Plan a retirement corpus fund well in advance which can enable you to move to an elderly care facility where you can have a dignified life.

Bottom line is , it is your life and your money. Only you have to plan it as none else would be interested in doing it for you without any personal interests. So take charge of your life, plan out things, work on a proper retirement plan and early financial independence so that you can spend your golden years in peace.

Recent Comments